Aevopedia - Chapter IV

Here you will find:

the last part of trading strategies

sources & individuals

how to get started

conclusions

^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^

What I write simply expresses my personal point of view and does not represent financial advice. But sure, beat me at beer pong and I will tell you the next 100x.

^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^

Hedging positions for the portfolio through the purchase of puts (currently available only for BTC and ETH) or opening shorts;

Yield bearing synthetic positions, both long and short, which can be obtained by combining two ATM option contracts of opposite type and side on platforms with noticeable price disparities. For example, by buying an ATM call and selling an ATM put with the same expiry, you get a payoff equivalent to owning 1 unit of the underlying asset. Conversely, if you sell a call and buy an ATM put with the same maturity, you get a payoff identical to someone opening short positions. Let me simplify this with an example:

— If on Lyra, I sell an ATM put (strike price 1950) on ETH with an expiration date of 24/11 for $48.71

— and then buy on Aevo an ATM call (strike price 1950) on ETH for $43.65..

...I will have a synthetic long position on ETH with an intrinsic gain at maturity (if nothing change in the meantime) of more than $5 per contract.

This position, over its lifetime, will have a delta equivalent to spot buying because it will lose/gain one point for every point lost/gained by the underlying.

This curious phenomenon is made possible by put-call parity, a rule that relates puts and calls with the same maturity and strike price and establishes an equivalence between these two instruments (if of opposite sign) and the underlying; the formula is as follows:

CALL — PUT = UNDERLYING — STRIKE

By relying on different platforms that apply Black-Scholes models different from each other, it is possible not only to open profitable synthetic positions (like the one in the example above) but also to carry out arbitrage operations if the premium received for selling one instrument is higher than the one spent to buy it back. To monitor arbitrage opportunities between premiums, I recommend using Stradle, which does not support Aevo but integrates data from all other platforms.

Sources (Links) & Individuals (Twitter handle)

Individuals

@juliankoh (co — founder)

@obadje_ (team member)

@chudnovglavniy (team member)

@kenchangh (Dev)

@Toppingthetop (one of the most active team members on discord, also known as Babbala, he is probably the community manager)

@0xcoffeebabe (Aevo TG bot creator)

Sources

Aevo product updates (TG channel)

Ribbon/Aevo Auction updates (TG channel)

How to get on board

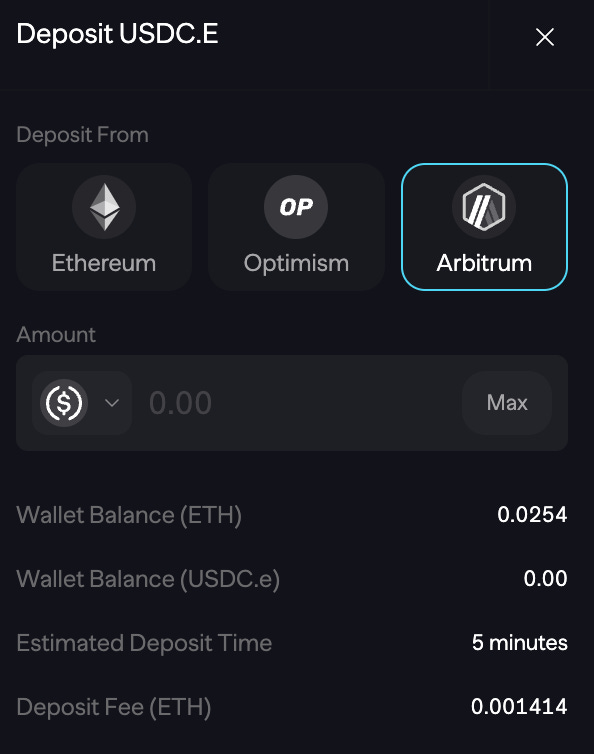

Interacting with the Aevo protocol is really simple and intuitive; to deposit, withdraw or transfer your funds to/from Aevo you need to visit the portfolio section and scroll down the page until you see the list of supported assets.

At this point choose the asset, click on the desired action (e.g. deposit), choose the network, enter the amount and finally confirm the transaction.

Conclusions

Aevo is one of the most fascinating protocols in its category. It boasts a team of highly competent individuals, offers a superior user experience (thanks to the gasless approach and the speed guaranteed by the custom OP rollup stack), and has one of the most advanced margin frameworks in the entire DeFi landscape.

The settlement in dollars without physical delivery at maturity sets it apart from the centralized competitor Deribit, configuring simpler payoff calculations.

The lack of transparent information about the financial status of the Insurance Fund and the names of market makers represents a drawback for the protocol, but positive developments in this direction could emerge soon.

Overall, the assessment is very positive, especially when considered in light of the "state of the art" on competitor products, which are progressing slowly or, at the very least, not at the same speed of Aevo.

Imho Lyra and Rysk (maybe also Premia) may have their slice of the options volume pie in DeFi but they need to close the gap asap.